Involuntary churn occurs when the subscriber doesn’t intend to cancel their subscription. It’s accidental.

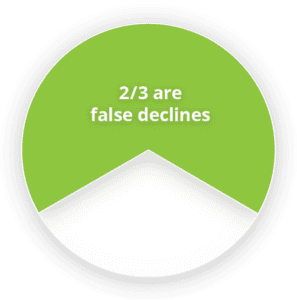

Data from Visa shows that 2/3 of card payment authorization declines are made in error and should have been approved.

Most subscription businesses make solving voluntary churn a priority and use specialized technology solutions. They implement voluntary churn reduction programs with dedicated team members who manage internal and customer-facing retention processes and systems. Or they create multi-function teams that jointly own the solutions, processes, and reporting systems dedicated to reducing churn. Voluntary churn is taken seriously, and increasing retention rates is viewed as a strategic imperative.

In-house solutions create a false sense of security, leading businesses to believe more effective solutions aren’t needed.

Payments fail for many reasons and need to be solved in a way that is most effective for each particular failure reason. In most cases, declines from bank errors and NSF can be solved directly with the payments system. But some failed payments, such as hard declines caused by cancelled or expired cards, will usually require customer involvement. No single method will solve all failed payments, so the top failed payment recovery solutions apply several technologies and approaches.

For example, the FlexPay failed payment recovery platform applies multiple approaches to solving failed payments. Our platform assesses each individual failed payment and uses AI to determine if recovery can be achieved by working directly with the payments system or if customer engagement is necessary. Solving the failed payment directly with the payments system is always preferred, because it avoids the risk of a negative brand experience. This can happen when a customer is aware of the failed payment. Our Invisible RecoveryTM solution creates a highly effective recovery strategy for each individual failed payment, working directly with the payments system. The customer never knows their payment failed.

Sometimes customer help is needed to solve the failed payment. Our Engaged RecoveryTM solution uses behavioral science to engage customers in a positive way across several channels, such as email and SMS. Every subscriber reacts differently to an outreach program, so Engaged Recovery applies multiple positive messaging approaches to find the one that prompts each customer to act. This approach maintains customer satisfaction and improves retention.