Recovering a failed payment is more than just recovering a transaction — the entire lifecycle of the customer before, during, and after recovery must be considered. How you treat the customer during this time can make or break your entire relationship. To ensure the customer remains a customer, your recovery process must be both technically effective — meaning the payment is recovered successfully — and the customer must go on to bill for many more months to achieve full LTV. Customer satisfaction must be your focus throughout the process.

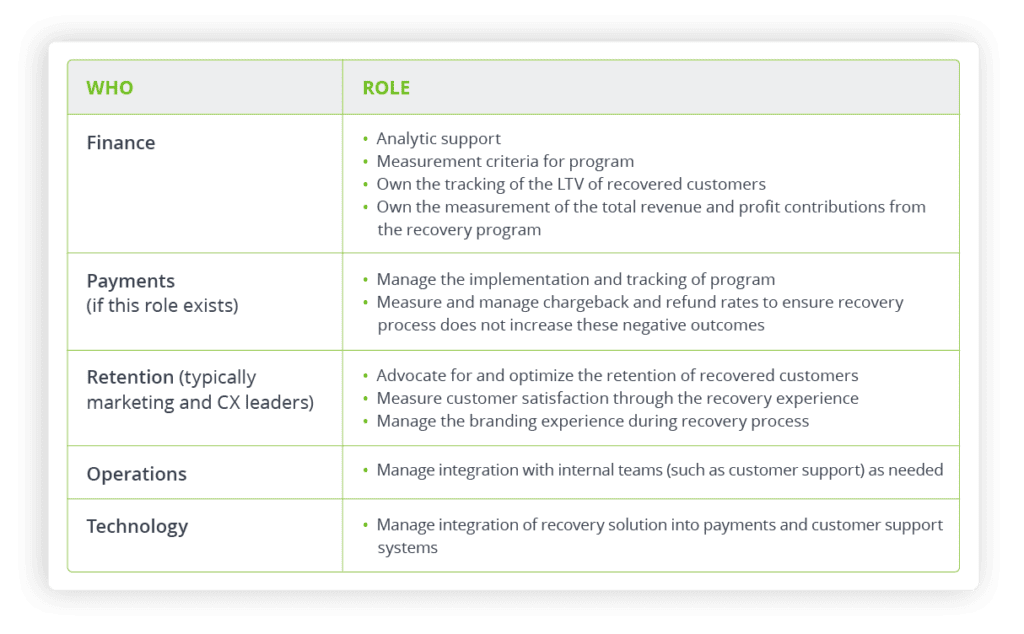

To do this, failed payment recovery should be a concern of everyone in the company and not viewed as simply a back end or a customer service responsibility. A cross-functional team made up of finance/payment experts, operations, technology, and CX/retention leaders should be created to solve the problem together with each team holding responsibility for a successful outcome. When people from across the company work together, it shows a deep understanding of just how important failed payment recovery is to the success of the business and it improves the likelihood of a successful recovery process.

When building out a recovery team, each member should represent their objectives and expertise so that the recovery solution, recovery experience, and retention following recovery are all measured, actively managed, and optimized. Here are the suggested members of an effective cross-functional payment recovery team and their individual responsibilities:

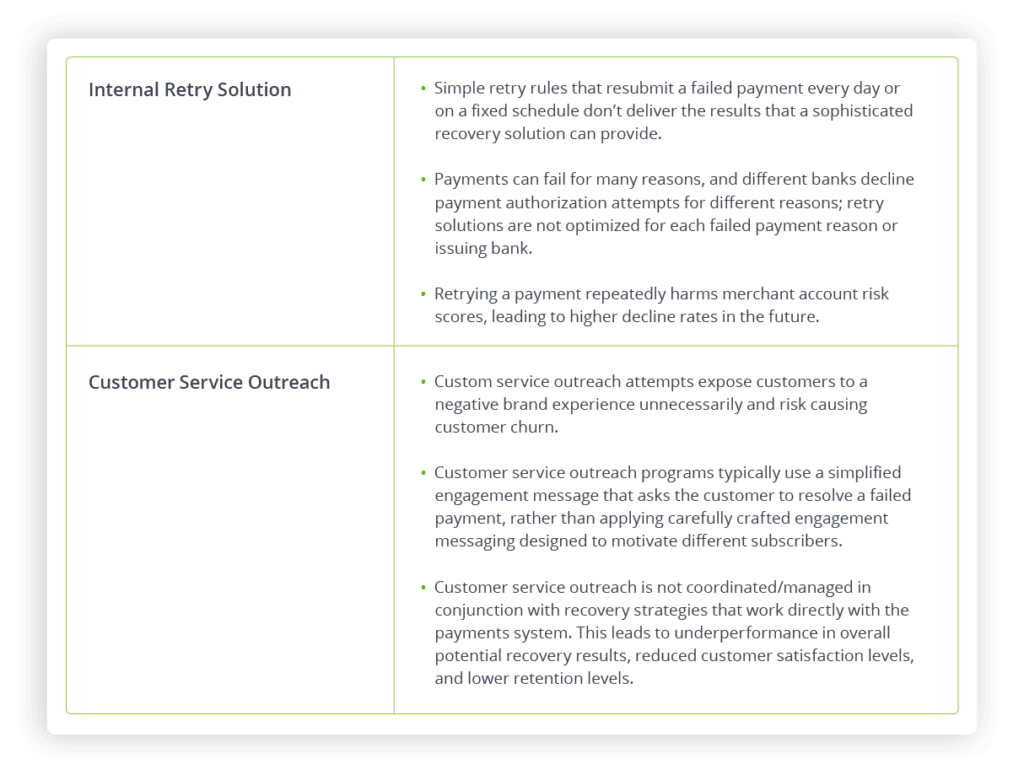

Many organizations build their own internal recovery solutions, often with the assumption that since they know their customers and their business best, they can build an effective recovery solution. These are good first steps to take, but internal solutions have performance limitations compared to the top specialized solutions, and they often cause unwanted challenges. The following chart summarizes the inherent limitations and unintended problems caused by internal solutions.